Tutorial¶

Introduction¶

Class vegas.Integrator gives Monte Carlo estimates of arbitrary

multidimensional integrals using the vegas algorithm

(G. P. Lepage, J. Comput. Phys. 27 (1978) 192 and J. Comput. Phys. 439 (2021) 110386).

The algorithm has two components.

First an automatic transformation is applied to to the integration variables

in an attempt to flatten the integrand. Then a Monte Carlo estimate of the

integral is made using the transformed variables. Flattening the integrand

makes the integral easier and improves the estimate. The transformation

applied to the integration variables is optimized

over several iterations of the algorithm: information about the integrand that

is collected during one iteration is used to improve the transformation used

in the next iteration.

Monte Carlo integration makes few assumptions about the integrand — it needn’t be analytic nor even continuous. This makes Monte Carlo integration unusually robust. It also makes it well suited for adaptive integration. Adaptive strategies are essential for multidimensional integration, especially in high dimensions, because multidimensional space is large, with lots of corners, making it easy to lose important features in the integrand.

Monte Carlo integration also provides efficient and reliable methods for estimating the accuracy of its results. In particular, each Monte Carlo estimate of an integral is a random number from a distribution whose mean is the correct value of the integral. This distribution is Gaussian or normal provided the number of integrand samples is sufficiently large. In practice we generate multiple estimates of the integral in order to verify that the distribution is indeed Gaussian. Error analysis is straightforward if the integral estimates are Gaussian.

The vegas algorithm has been in use for decades and implementations are

available in many programming languages, including Fortran (the original

version), C and C++. The algorithm used here is significantly improved over

the original implementation, and that used in most other implementations.

It uses two adaptive strategies: importance sampling, as in the original

implementation, and adaptive stratified sampling, which is new. The

new algorithm is described in G. P. Lepage, arXiv_2009.05112

(J. Comput. Phys. 439 (2021) 110386).

There is also a third adaptive strategy, adaptive re-stratification, that can

be useful in very high dimensions. See vegas.restratify().

This module is written in Cython, so it is almost as fast as compiled Fortran or C, particularly when the integrand is also coded in Cython (or some other compiled language), as discussed below.

The following sections describe how to use vegas. Almost every

example shown is a complete code, which can be copied into a file

and run with Python. It is worthwhile playing with the parameters to see how

things change.

About Printing: The examples in this tutorial use the print function as it is used in Python 3. Drop the outermost parenthesis in each print statement if using Python 2, or add

from __future__ import print_function

at the start of your file.

Basic Integrals¶

Here we illustrate the use of vegas by estimating the integral

where constant  is chosen so that the exact integral is 1.

The following code shows how this can be done:

is chosen so that the exact integral is 1.

The following code shows how this can be done:

import vegas

import math

def f(x):

dx2 = 0

for d in range(4):

dx2 += (x[d] - 0.5) ** 2

return math.exp(-dx2 * 100.) * 1013.2118364296088

integ = vegas.Integrator([[-1, 1], [0, 1], [0, 1], [0, 1]])

result = integ(f, nitn=10, neval=1000)

print(result.summary())

print('result = %s Q = %.2f' % (result, result.Q))

First we define the integrand f(x) where x[d] specifies a point in the

4-dimensional space. We then create an integrator, integ, which is an

integration operator that can be applied to any 4-dimensional function. It is

where we specify the integration volume.

Finally we apply integ to our integrand f(x),

telling the integrator to estimate the integral using nitn=10 iterations

of the vegas algorithm, each of which uses no more than neval=1000

evaluations of the integrand. Each iteration produces an independent

estimate of the integral. The final estimate is the weighted average of

the results from all 10 iterations, and is returned by integ(f ...).

The call result.summary() returns

a summary of results from each iteration.

This code produces the following output:

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 2.6(1.4) 2.6(1.4) 0.00 1.00

2 1.32(25) 1.36(25) 0.75 0.39

3 0.909(96) 0.968(89) 1.79 0.17

4 1.039(69) 1.012(55) 1.32 0.26

5 0.929(34) 0.952(29) 1.41 0.23

6 1.003(26) 0.980(19) 1.47 0.20

7 0.994(18) 0.988(13) 1.27 0.27

8 0.998(14) 0.9922(98) 1.13 0.34

9 1.020(12) 1.0035(75) 1.39 0.20

10 1.011(12) 1.0057(64) 1.27 0.25

result = 1.0057(64) Q = 0.25

There are several things to note here:

Adaptation: Integration estimates are shown for each of the 10 iterations, giving both the estimate from just that iteration, and the weighted average of results from all iterations up to that point. The estimates from the first two iterations are not accurate at all, with errors equal to 25–140% of the final result.

vegasinitially has no information about the integrand and so does a relatively poor job of estimating the integral. It uses information from the samples in one iteration, however, to remap the integration variables for subsequent iterations, concentrating samples where the function is largest and reducing errors. As a result, the per-iteration error is reduced to 3.4% by the fifth iteration, and almost to 1% by the end — an improvement by a factor of more than 100 from the start. Eventually the per-iteration error stops decreasing becausevegashas found the optimal remapping, at which point it is fully adapted to the integrand.Weighted Average: The final result, 1.0057 ± 0.0064, is obtained from a weighted average of the separate results from each iteration: estimates are weighted by the inverse variance, thereby giving much less weight to the early iterations, where the errors are largest. The individual estimates are statistical: each is a random number drawn from a distribution whose mean equals the correct value of the integral, and the errors quoted are estimates of the standard deviations of those distributions. The distributions are Gaussian provided the number of integrand evaluations per iteration (

neval) is sufficiently large, in which case the standard deviation is a reliable estimate of the error. The weighted averageminimizes

where

are the estimates from individual iterations. If the

are Gaussian,

should be of order the number of degrees of freedom (plus or minus the square root of double that number); here the number of degrees of freedom is the number of iterations minus 1.

The distributions are likely non-Gaussian, and error estimates unreliable, if

nevalis not sufficiently large to guarantee Gaussian behavior, and must be increased if the error estimates are to be trusted.

integ(f...)returns a weighted-average object, of typevegas.RAvg, that has the following attributes:

result.mean— weighted average of all estimates of the integral;

result.sdev— standard deviation of the weighted average;

result.chi2—

result.dof— number of degrees of freedom;

result.Q— Q or p-value of the weighted average’s

result.itn_results— list of the integral estimates from each iteration;

result.sum_neval— total number of integrand evaluations used.

result.avg_neval— average number of integrand evaluations per iterationIn this example the final Q is 0.25, indicating that the

Precision: The precision of

vegasestimates is determined bynitn, the number of iterations of thevegasalgorithm, and byneval, the maximum number of integrand evaluations made per iteration. The computing cost is typically proportional to the product ofnitnandneval. The number of integrand evaluations per iteration varies from iteration to iteration, here between 860 and 960. Typicallyvegasneeds more integration points in early iterations, before it has fully adapted to the integrand.We can increase precision by increasing either

nitnorneval, but it is generally far better to increaseneval. For example, adding the following lines to the code aboveresult = integ(f, nitn=100, neval=1000) print('larger nitn => %s Q = %.2f' % (result, result.Q)) result = integ(f, nitn=10, neval=1e4) print('larger neval => %s Q = %.2f' % (result, result.Q))generates the following results:

larger nitn => 1.0003(13) Q = 0.79 larger neval => 0.99981(53) Q = 0.28The total number of integrand evaluations,

nitn * neval, is about the same in both cases, but increasingnevalis more than twice as accurate as increasingnitn. Typically you want to use no more than 10 or 20 iterations beyond the point wherevegashas fully adapted. You want some number of iterations so that you can verify Gaussian behavior by checking theIt is also generally useful to compare two or more results from values of

nevalthat differ by a significant factor (4–10, say). These should agree within errors. If they do not, it could be due to non-Gaussian artifacts caused by a smallneval.vegasestimates have two sources of error. One is the statistical error, which is what is quoted byvegas. The other is a systematic error due to residual non-Gaussian effects. The systematic error vanishes like1/nevalor faster, and so becomes negligible compared with the statistical error asnevalincreases. The systematic error can bias the Monte Carlo estimate, however, ifnevalis insufficiently large. This usually results in a largeneval. The systematic errors due to non-Gaussian behavior are likely negligible if the different estimates agree to within the statistical errors.The possibility of systematic biases is another reason for increasing

nevalrather thannitnto obtain more precision. Makingnevallarger and larger is guaranteed to improve the Monte Carlo estimate, as the statistical error decreases and the systematic error decreases even more quickly. Makingnitnlarger and larger, on the other hand, is guaranteed eventually to give the wrong answer. This is because at some point the statistical error (which falls assqrt(1/nitn)) will no longer mask the systematic error (which is unaffected bynitn). The systematic error for the integral above (withneval=1000) is about -0.0008, which is negligible compared to the statistical error unlessnitnis of order 1500 or larger — so systematic errors aren’t a problem withnitn=10.Early Iterations: Integral estimates from early iterations, before

vegashas adapted, can be quite crude. With very peaky integrands, these are often far from the correct answer with highly unreliable error estimates. For example, the integral above becomes more difficult if we double the length of each side of the integration volume by redefiningintegas:integ = vegas.Integrator([[-2, 2], [0, 2], [0, 2], [0., 2]])The code above then gives:

itn integral wgt average chi2/dof Q ------------------------------------------------------- 1 0.0011(10) 0.0011(10) 0.00 1.00 2 0.074(56) 0.0011(10) 1.71 0.19 3 0.250(59) 0.0012(10) 9.65 0.00 4 0.93(14) 0.0013(10) 21.40 0.00 5 0.874(70) 0.0015(10) 54.87 0.00 6 0.949(39) 0.0021(10) 162.08 0.00 7 0.949(30) 0.0033(10) 301.18 0.00 8 0.985(25) 0.0050(10) 484.50 0.00 9 0.967(19) 0.0078(10) 738.53 0.00 10 0.988(15) 0.0125(10) 1131.46 0.00 result = 0.0125(10) Q = 0.00

vegasmisses the peak completely in the first iteration, giving an estimate that is completely wrong (by 1000 standard deviations!). Some of its samples hit the peak’s shoulders, sovegasis eventually able to find the peak (by iterations 5–6), but the integrand estimates are wildly non-Gaussian before that point. This results in a nonsensical final result, as indicated by theQ = 0.00.It is common practice in using

vegasto discard estimates from the first several iterations, before the algorithm has adapted, in order to avoid ruining the final result in this way. This is done by replacing the single call tointeg(f...)in the original code with two calls:# step 1 -- adapt to f; discard results integ(f, nitn=10, neval=1000) # step 2 -- integ has adapted to f; keep results result = integ(f, nitn=10, neval=1000) print(result.summary()) print('result = %s Q = %.2f' % (result, result.Q))The integrator is trained in the first step, as it adapts to the integrand, and so is more or less fully adapted from the start in the second step, which yields:

itn integral wgt average chi2/dof Q ------------------------------------------------------- 1 0.993(17) 0.993(17) 0.00 1.00 2 1.062(48) 1.001(16) 1.83 0.18 3 0.964(20) 0.987(13) 1.91 0.15 4 0.974(16) 0.9817(99) 1.40 0.24 5 0.990(15) 0.9843(82) 1.10 0.35 6 1.012(16) 0.9899(73) 1.34 0.25 7 0.999(15) 0.9917(65) 1.16 0.32 8 1.008(12) 0.9953(58) 1.20 0.30 9 1.013(15) 0.9977(54) 1.20 0.29 10 0.983(14) 0.9958(50) 1.17 0.31 result = 0.9958(50) Q = 0.31The final result is now reliable.

Other Integrands: Once

integhas been trained onf(x), it can be usefully applied to other functions with similar structure. For example, adding the following at the end of the original code,def g(x): return x[0] * f(x) result = integ(g, nitn=10, neval=1000) print(result.summary()) print('result = %s Q = %.2f' % (result, result.Q))gives the following new output:

itn integral wgt average chi2/dof Q ------------------------------------------------------- 1 0.4933(61) 0.4933(61) 0.00 1.00 2 0.5017(54) 0.4980(40) 1.04 0.31 3 0.4975(64) 0.4979(34) 0.52 0.59 4 0.5059(60) 0.4998(30) 0.80 0.49 5 0.5075(64) 0.5012(27) 0.90 0.46 6 0.4907(66) 0.4997(25) 1.15 0.33 7 0.5009(47) 0.5000(22) 0.97 0.45 8 0.5082(58) 0.5010(21) 1.08 0.38 9 0.5016(63) 0.5010(20) 0.94 0.48 10 0.4934(76) 0.5006(19) 0.94 0.49 result = 0.5006(19) Q = 0.49Again the grid is almost optimal for

g(x)from the start, becauseg(x)peaks in the same region asf(x). The exact value for this integral is very close to 0.5.Non-Rectangular Volumes:

vegascan integrate over volumes of non-rectangular shape. For example, we can replace integrandf(x)above by the same Gaussian, but restricted to a 4-sphere of radius 0.2, centered on the Gaussian:import vegas import math def f_sph(x): dx2 = 0 for d in range(4): dx2 += (x[d] - 0.5) ** 2 if dx2 < 0.2 ** 2: return math.exp(-dx2 * 100.) * 1115.3539360527281318 else: return 0.0 integ = vegas.Integrator([[-1, 1], [0, 1], [0, 1], [0, 1]]) integ(f_sph, nitn=10, neval=1000) # adapt the grid result = integ(f_sph, nitn=10, neval=1000) # estimate the integral print(result.summary()) print('result = %s Q = %.2f' % (result, result.Q))The normalization is adjusted to again make the exact integral equal 1. Integrating as before gives:

itn integral wgt average chi2/dof Q ------------------------------------------------------- 1 0.992(20) 0.992(20) 0.00 1.00 2 0.993(19) 0.992(14) 0.00 0.97 3 1.002(18) 0.996(11) 0.09 0.91 4 1.004(22) 0.9973(98) 0.10 0.96 5 1.026(30) 1.0001(93) 0.28 0.89 6 1.053(92) 1.0007(93) 0.29 0.92 7 1.035(30) 1.0038(89) 0.45 0.85 8 0.991(19) 1.0014(80) 0.44 0.88 9 0.968(18) 0.9956(73) 0.76 0.64 10 1.022(37) 0.9966(72) 0.73 0.68 result = 0.9966(72) Q = 0.68It is a good idea to make the actual integration volume as large a fraction as possible of the total volume used by

vegas— by choosing integration variables properly — sovegasdoesn’t spend lots of effort on regions where the integrand is exactly 0. Also, it can be challenging forvegasto find the region of non-zero integrand in high dimensions: integratingf_sph(x)in 20 dimensions instead of 4, for example, would requireneval=1e16integrand evaluations per iteration to have any chance of finding the region of non-zero integrand, because the volume of the 20-dimensional sphere is a tiny fraction of the total integration volume. The final error in the example above would have been cut in half had we used the integration volume4 * [[0.3, 0.7]]instead of[[-1, 1], [0, 1], [0, 1], [0, 1]].Note, finally, that integration to infinity is also possible: map the relevant variable into a different variable of finite range. For example, an integral over

from 0 to infinity is easily re-expressed as an integral over

from 0 to 1, where the transformation emphasizes the region in

of order free parameter

.

Damping: The result in the previous section can be improved somewhat by slowing down

vegas’s adaptation:... integ(f_sph, nitn=10, neval=1000, alpha=0.1) result = integ(f_sph, nitn=10, neval=1000, alpha=0.1) ...Parameter

alphacontrols the speed with whichvegasadapts, with smalleralphas giving slower adaptation. Here we reducealphato 0.1, from its default value of 0.5, and get the following output:itn integral wgt average chi2/dof Q ------------------------------------------------------- 1 1.008(26) 1.008(26) 0.00 1.00 2 0.993(23) 0.999(17) 0.19 0.66 3 1.005(21) 1.002(13) 0.11 0.89 4 1.016(20) 1.006(11) 0.19 0.91 5 0.973(18) 0.9967(95) 0.73 0.57 6 1.016(18) 1.0009(84) 0.77 0.57 7 1.008(18) 1.0023(76) 0.66 0.68 8 0.990(17) 1.0002(69) 0.63 0.73 9 1.008(17) 1.0012(64) 0.58 0.80 10 0.958(17) 0.9959(60) 1.12 0.34 result = 0.9959(60) Q = 0.34Notice how the errors fluctuate less from iteration to iteration with the smaller

alphain this case. Persistent, large fluctuations in the size of the per-iteration errors is often a signal thatalphashould be reduced. With largeralphas,vegascan over-react to random fluctuations it encounters as it samples the integrand.In general, we want

alphato be large enough so thatvegasadapts quickly to the integrand, but not so large that it has difficulty holding on to the optimal tuning once it has found it. The best value depends upon the integrand.adapt=False: Adaptation can be turned off completely by setting parameter

adapt=False. There are three reasons one might do this. The first is ifvegasis exhibiting the kind of instability discussed in the previous section — one might use the following code, instead of that presented there:... integ(f_sph, nitn=10, neval=1000, alpha=0.1) result = integ(f_sph, nitn=10, neval=1000, adapt=False) ...The second reason is that

vegasruns slightly faster when it is no longer adapting to the integrand. The difference is not signficant for complicated integrands, but is noticable in simpler cases.The third reason for turning off adaptation is that

vegasuses unweighted averages, rather than weighted averages, to combine results from different iterations whenadapt=False. Unweighted averages are not biased. They have no systematic error of the sort discussed above, and so give correct results even for very large numbers of iterations,nitn.The lack of systematic biases is not a strong reason for turning off adaptation, however, since the biases are usually negligible (see above). The most important reason is the first: stability.

adapt=Falseis particularly useful when the number of integrand evaluationsnevalis small for the integrand, leading to large fluctuations in the errors from iteration to iteration. For example, the following output is from an estimate (withneval=2.5e4) of an eight-dimensional integral with three sharp peaks along the diagonal (Eq. (45) in arXiv_2009.05112, normalized so that the correct answer equals 1):itn integral wgt average chi2/dof Q ------------------------------------------------------- 1 0.75(43) 0.75(43) 0.00 1.00 2 0.506(58) 0.510(58) 0.32 0.57 3 0.80(21) 0.530(56) 1.02 0.36 4 0.76(11) 0.576(50) 1.81 0.14 5 1.27(29) 0.596(49) 2.74 0.03 6 1.10(19) 0.629(48) 3.56 0.00 7 0.802(73) 0.681(40) 3.63 0.00 8 2.8(2.0) 0.681(40) 3.27 0.00 9 0.907(90) 0.719(36) 3.52 0.00 10 1.07(16) 0.736(35) 3.65 0.00 itn integral average chi2/dof Q ------------------------------------------------------- 1 1.13(14) 1.13(14) 0.00 1.00 2 1.064(96) 1.095(86) 0.13 0.72 3 1.03(10) 1.072(67) 0.19 0.83 4 0.924(94) 1.035(55) 0.58 0.63 5 0.858(71) 1.000(46) 1.08 0.37 6 0.97(11) 0.995(43) 0.84 0.52 7 0.924(69) 0.985(38) 0.84 0.54 8 1.19(16) 1.010(39) 1.01 0.42 9 1.74(73) 1.092(88) 1.01 0.42 10 0.942(89) 1.077(80) 1.02 0.42The first 10 iterations are used to train the

vegasmap; their results are discarded. The next 10 iterations, withadapt=False, have uncertainties that fluctuate in size by an order of magnitude, but still give a reliable estimate for the integral (1.08(8)). Allowingvegasto continue adapting in the the second set of iterations gives results like 0.887(25), which is 4.5 standard deviations too low; the real uncertainty is larger than ±0.025.Training the integrator and then setting

adapt=Falsefor the final results works best if the number of evaluations per iteration (neval) is the same in both steps. This is because the second ofvegas’s adaptation strategies (Adaptive Stratified Sampling) is usually reinitialized whennevalchanges, and so is not used at all whennevalis changed at the same timeadapt=Falseis set.

Multiple Integrands Simultaneously¶

vegas can be used to integrate multiple integrands simultaneously, using

the same integration points for each of the integrands. This is useful

in situations where the integrands have similar structure, with peaks in

the same locations. There can be signficant advantages in sampling

different integrands at precisely the same points in x space, because

then Monte Carlo estimates for the different integrals are correlated.

If the integrands are very similar to each other, the correlations can be

very strong. This leads to greatly reduced errors in ratios or differences

of the resulting integrals as the fluctuations cancel.

Consider a simple example. We want to compute the normalization and first two moments of a sharply peaked probability distribution:

From these integrals we determine the mean and width of the distribution projected onto one of the axes:

![\langle x \rangle &\equiv I_1 / I_0 \\[1ex]

\sigma_x^2 &\equiv \langle x^2 \rangle - \langle x \rangle^2 \\

&= I_2 / I_0 - (I_1 / I_0)^2](_images/math/8a2f87c47c9a6ee77d7e8f816eada511053bee65.svg)

This can be done using the following code:

import vegas

import math

import gvar as gv

def f(x):

dx2 = 0.0

for d in range(4):

dx2 += (x[d] - 0.5) ** 2

f = math.exp(-200 * dx2)

return [f, f * x[0], f * x[0] ** 2]

integ = vegas.Integrator(4 * [[0, 1]])

# adapt grid

training = integ(f, nitn=10, neval=2000)

# final analysis

result = integ(f, nitn=10, neval=10000)

print('I[0] =', result[0], ' I[1] =', result[1], ' I[2] =', result[2])

print('Q = %.2f\n' % result.Q)

print('<x> =', result[1] / result[0])

print(

'sigma_x**2 = <x**2> - <x>**2 =',

result[2] / result[0] - (result[1] / result[0]) ** 2

)

print('\ncorrelation matrix:\n', gv.evalcorr(result))

The code is very similar to that used in the previous section. The

main difference is that the integrand function and vegas

return arrays of results — in

both cases, one result for each of the three integrals. vegas always adapts to

the first integrand in the array. The Q value is for all three

of the integrals, taken together.

The code produces the following output:

I[0] = 0.00024682(12) I[1] = 0.000123417(61) I[2] = 0.000062327(33)

Q = 0.93

<x> = 0.500017(49)

sigma_x**2 = <x**2> - <x>**2 = 0.0024983(73)

correlation matrix:

[[1. 0.98002885 0.92558296]

[0.98002885 1. 0.98157932]

[0.92558296 0.98157932 1. ]]

The estimates for the individual integrals are separately accurate to

about ±0.05%,

but the estimate for  is accurate to ±0.01%.

This is almost an order

of magnitude (8x) more accurate than we would obtain absent correlations.

The correlation matrix shows that there is 98% correlation between the

statistical fluctuations in estimates for

is accurate to ±0.01%.

This is almost an order

of magnitude (8x) more accurate than we would obtain absent correlations.

The correlation matrix shows that there is 98% correlation between the

statistical fluctuations in estimates for  and

and  ,

and so the bulk of these fluctuations cancel in the ratio.

The estimate for the variance

,

and so the bulk of these fluctuations cancel in the ratio.

The estimate for the variance  is 48x more accurate than we would

have obtained had the integrals been evaluated separately. Both estimates

are correct to within the quoted errors.

is 48x more accurate than we would

have obtained had the integrals been evaluated separately. Both estimates

are correct to within the quoted errors.

The individual results are objects of type gvar.GVar, which

represent Gaussian random variables. Such objects have means

(result[i].mean) and standard deviations (result[i].sdev), but

also can be statistically correlated with other gvar.GVars.

Such correlations are handled automatically by gvar when

gvar.GVars are combined with each other or with numbers in

arithmetical expressions. (Documentation for gvar can be found

at https://gvar.readthedocs.io or with the source code

at https://github.com/gplepage/gvar.git.)

Dictionaries¶

Integrands can return dictionaries instead of arrays. The example in the previous section, for example, can be rewritten as

import vegas

import math

import gvar as gv

def f(x):

dx2 = 0.0

for d in range(4):

dx2 += (x[d] - 0.5) ** 2

f = math.exp(-200 * dx2)

return {'1':f, 'x':f * x[0], 'x**2':f * x[0] ** 2}

integ = vegas.Integrator(4 * [[0, 1]])

# adapt grid

training = integ(f, nitn=10, neval=2000)

# final analysis

result = integ(f, nitn=10, neval=10000)

print(result)

print('Q = %.2f\n' % result.Q)

print('<x> =', result['x'] / result['1'])

print(

'sigma_x**2 = <x**2> - <x>**2 =',

result['x**2'] / result['1'] - (result['x'] / result['1']) ** 2

)

which returns the following output:

{'1': 0.00024682(12),'x': 0.000123417(61),'x**2': 0.000062327(33)}

Q = 0.93

<x> = 0.500017(49)

sigma_x**2 = <x**2> - <x>**2 = 0.0024983(73)

The result returned by vegas is a dictionary using the same keys as the

dictionary returned by the integrand. Using a dictionary with descriptive

keys, instead of an array, can often make code more intelligible, and,

therefore, easier to write and maintain. Here the values in the integrand’s

dictionary are all numbers; in general, values can be either numbers or

arrays (of any shape).

Dictionaries can also be used for the integration variables. For example, the following code calculates the volume of a unit sphere using spherical coordinates:

import numpy as np

import vegas

def f(xd):

r = xd['r']

theta = xd['theta']

phi = xd['phi']

return r ** 2 * np.sin(theta)

integ = vegas.Integrator(dict(r=(0,1), theta=(0, np.pi), phi=(0, 2 * np.pi)))

volume = integ(f, neval=1000, nitn=10)

print(volume)

Running this code gives a result of 4.1852(44) which agrees well (0.1%) with the correct

result  . This can be generalized to

. This can be generalized to DIM dimensions,

where now xd['phi'] is an array of variables: e.g.,

import numpy as np

import vegas

DIM = 5

def f(xd):

r = xd['r']

phi = xd['phi']

# construct Euclidean coordinates, Jacobian

x = np.zeros(DIM, float)

x[:] = r

x[1:] *= np.cumprod(np.sin(phi), axis=0)

jac = np.prod(x[1:-1], axis=0) * r

x[:-1] *= np.cos(phi)

# calculate contribution to sphere's volume

return jac

integ = vegas.Integrator(dict(

r=(0,1),

phi=(DIM - 2) * [(0, np.pi)] + [(0, 2 * np.pi)]

))

warmup = integ(f, neval=1000, nitn=10)

volume = integ(f, neval=1000, nitn=10)

print(integ.settings(), '\n')

print(f'volume(dim={DIM}) = {volume}')

This code generates the following output:

Integrator Settings:

1000 (approx) integrand evaluations in each of 10 iterations

number of: strata/axis = [3 3 3 2 2]

increments/axis = [ 99 99 99 100 100]

h-cubes = 108 processors = 1

evaluations/batch >= 5e+04

2 <= evaluations/h-cube <= 5e+04

minimize_mem = False adapt_to_errors = False adapt = True

accuracy: relative = 0 absolute = 0

damping: alpha = 0.5 beta= 0.75

key/index axis integration limits

---------------------------------------------

r 0 (0.0, 1.0)

phi 0 1 (0.0, 3.141592653589793)

1 2 (0.0, 3.141592653589793)

2 3 (0.0, 3.141592653589793)

3 4 (0.0, 6.283185307179586)

volume(dim=5) = 5.254(12)

Calculating Distributions¶

vegas is often used to calculate distributions. The following

code, for example, evaluates both an integral I and the contributions

dI to the integral coming from each of five different intervals dr

in the radius measured

from the center of the integration volume. The normalized contributions

dI/I are then tabulated:

import vegas

import numpy as np

RMAX = (2 * 0.5**2) ** 0.5

def fcn(x):

dx2 = 0.0

for d in range(2):

dx2 += (x[d] - 0.5) ** 2

I = np.exp(-dx2)

# add I to appropriate bin in dI

dI = np.zeros(5, dtype=float)

dr = RMAX / len(dI)

j = int(dx2 ** 0.5 / dr)

dI[j] = I

return dict(I=I, dI=dI)

integ = vegas.Integrator(2 * [(0,1)])

# results returned in a dictionary

result = integ(fcn)

print(result.summary())

print(' I =', result['I'])

print('dI/I =', result['dI'] / result['I'])

print('sum(dI/I) =', sum(result['dI']) / result['I'])

Note the check at the end, to verify that the sum of the

dI[i]s equals the original integral. Running this script gives

the following output:

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 0.85040(55) 0.85040(55) 0.00 1.00

2 0.85039(45) 0.85040(35) 0.76 0.60

3 0.85085(39) 0.85061(26) 0.63 0.82

4 0.85105(33) 0.85079(20) 0.52 0.95

5 0.85105(30) 0.85087(17) 0.60 0.94

6 0.85097(24) 0.85091(14) 0.55 0.98

7 0.85099(21) 0.85096(11) 0.72 0.90

8 0.85112(17) 0.851013(93) 0.66 0.95

9 0.85114(15) 0.851053(79) 0.70 0.94

10 0.85101(13) 0.851041(67) 0.68 0.96

I = 0.851041(67)

dI/I = [0.0759(12) 0.2091(23) 0.3217(27) 0.3209(23) 0.0723(12)]

sum(dI/I) = 0.999999999996(26)

The integrator adapts to the full integral I but also gives

accurate results for the distribution dI (though not quite as

accurate). Note that sum(dI/I) is much more accurate than

any individual dI/I, because of correlations between

the different dI/I values. (The uncertainty on sum(dI/I) would

be exactly zero absent roundoff errors.)

Often one has more than five bins in a distribution. Increasing the number to 100 in the example above reveals a problem:

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 0.85040(55) 0.85040(55) 0.00 1.00

2 0.85039(45) 0.85079(39) 0.75 0.97

3 0.85085(39) 0.820(49) 0.73 1.00

4 0.85105(33) 0.813(40) 0.81 0.99

5 0.85105(30) 0.837(24) 0.96 0.73

6 0.85097(24) 0.85236(75) 1.10 0.06

7 0.85099(21) 0.85242(25) 1.19 0.00

8 0.85112(17) 0.85242(23) 1.22 0.00

9 0.85114(15) 0.85234(21) 1.22 0.00

10 0.85101(13) 0.85179(11) 1.25 0.00

I = 0.85179(11)

dI/I = [0.00012(87) 0.00177(62) 0.00016(83) 0.00067(51) 0.00103(53)...]

sum(dI/I) = 1.0000117(35)

Something is going wrong with the weighted averages of the results from different iterations, as is clear by the third iteration. The weights used in the weighted average are obtained from the inverse of the covariance matrix for the different components of the integral — here a 101×101 matrix. This matrix becomes quite singular as it grows, and therefore is quite sensitive to even small errors in the covariance matrix. These errors, particularly in early iterations, can introduce large errors in the weighted averages.

This problem can be addressed by increasing the number of integrand

evaluations per iteration neval, which increases the accuracy

of the Monte Carlo estimate of the covariance matrix. A more efficient

solution in this case, however, is to break the integration into two parts: one

where the integrator is adapted to the integrand, but the results

are discarded; and a second step where adaptation is turned off

with adapt=False to obtain the final result. As discussed above,

vegas does not use a weighted average when adapt=False and

so the inversion of the covariance matrices is unnecessary.

To implement this strategy in the code above, replace the line

result = integ(fcn)

with

discard = integ(fcn) # adapt to grid

result = integ(fcn, adapt=False) # no further adaptation

This gives the following output:

itn integral average chi2/dof Q ------------------------------------------------------- 1 0.85113(11) 0.85113(11) 0.00 1.00 2 0.85113(12) 0.851130(81) 0.99 0.50 3 0.85124(11) 0.851166(65) 1.08 0.21 4 0.85129(11) 0.851197(56) 1.04 0.31 5 0.85105(12) 0.851168(51) 0.99 0.54 6 0.85120(11) 0.851173(46) 0.99 0.57 7 0.85114(11) 0.851169(43) 0.98 0.63 8 0.85107(11) 0.851156(40) 1.03 0.29 9 0.85114(11) 0.851154(37) 1.04 0.19 10 0.85110(11) 0.851149(36) 1.02 0.31 I = 0.851149(36) dI/I = [0.00034(24) 0.00067(34) 0.00067(34) 0.00185(49) 0.00101(39)...] sum(dI/I) = 1.000000000000(37)

The correct result for I is 0.85112.

PDF Integrals¶

The vegas module has a special-purpose integrator for

evaluating averages over probability distributions.

In its simplest form,

g_ev = vegas.PDFIntegrator(param=g)

creates an integrator optimized for the multi-dimensional Gaussian

probability distribution corresponding to g. (g is

an array of Gaussian random variables of type gvar.GVar,

or a dictionary whose

values are gvar.GVars or arrays of gvar.GVars.)

Then g_ev(f) evaluates the expectation value of a

function f(p) with respect to this distribution,

where p is a point in the distribution’s parameter

space.

More generally

pdf_ev = vegas.PDFIntegrator(param=g, pdf=pdf)

creates an integrator which calculates expectation values with

respect to an arbitrary probability density function pdf(p).

The parameter space for points p is again defined by

and optimized for the PDF corresponding to g, but

expectation values are calculated with pdf(p). Typically

g’s means and covariance would be chosen to emphasize

the regions where pdf(p) is large (e.g., g might be

set equal to the prior in a Bayesian analysis).

In general, the integrator uses param to define and optimize the

internal integration parameters. It re-expresses integrals in

terms of variables

that diagonalize param’s correlation matrix and are centered at

its mean value. This greatly facilitates integration over these

variables using vegas, making integrals over

many parameters feasible, even when the parameters are highly

correlated. vegas.PDFIntegrator also pre-adapts the integrator

to param’s PDF so it is often unnecessary to discard early iterations.

vegas.PDFIntegrator evaluates the

integrals of both pdf(p) * f(p) and pdf(p). The expectation

value is the ratio of the two integrals, so the PDF need not be

normalized. Note also that Monte Carlo uncertainties in

the two integrals are often highly correlated, in which case

the uncertainties are significantly reduced in the ratio.

A simple illustration of vegas.PDFIntegrator is given by the following

code, where g determines both the parameterization of the integrals

and the PDF used for expectation values:

import vegas

import gvar as gv

# multi-dimensional distribution

g = gv.BufferDict()

g['a'] = gv.gvar([2., 1.], [[1., 0.99], [0.99, 1.]])

g['fb(b)'] = gv.BufferDict.uniform('fb', 0.0, 2.0)

# integrator for expectation values in distribution g

g_ev = vegas.PDFIntegrator(g)

# adapt integrator to the PDF

g_ev(neval=10_000, nitn=5)

# want expectation value of [fp, fp**2]

def f_f2(p):

a = p['a']

b = p['b']

fp = a[0] * a[1] + 3 * b

return [fp, fp ** 2]

# <f_f2> in distribution g

r = g_ev(f_f2, adapt=False)

print(r.summary())

print('results =', r, '\n')

# mean and standard deviation of fp's distribution

fmean = r[0]

fsdev = gv.sqrt(r[1] - r[0] ** 2)

print ('fp.mean =', fmean, ' fp.sdev =', fsdev)

print ("Gaussian approx'n for fp =", f_f2(g)[0], '\n')

# g's pdf norm

print('PDF norm =', r.pdfnorm)

Here the distribution g describes two highly correlated Gaussian

variables, a[0] and a[1], and a third uncorrelated variable b

that is uniformly distributed on the interval [0,2] (see the gvar

documentation for more information).

We use the integrator to calculated the expectation value of

fp = a[0]*a[1] + 3*b and fp**2, so we can compute the

mean and standard

deviation of the fp distribution. The output from this code

shows that the Gaussian approximation 5.0(3.8) for the mean and

standard deviation is not particularly

close to the correct value 6.0(3.8):

itn integral average chi2/dof Q

-------------------------------------------------------

1 0.9995(11) 0.9995(11) 0.00 1.00

2 1.0011(11) 1.00030(78) 0.36 0.78

3 1.0013(12) 1.00062(65) 0.31 0.93

4 1.0003(10) 1.00055(55) 0.24 0.99

5 1.0000(11) 1.00044(50) 0.45 0.94

results = [5.9996(54) 50.09(15)]

fp.mean = 5.9996(54) fp.sdev = 3.755(13)

Gaussian approx'n for fp = 5.0(3.8)

PDF norm = 1.00044(50)

In general the function f(p) in g_ev(f) can return a number,

or an array of

numbers, or a dictionary whose values are numbers or arrays of numbers.

This allows multiple expectation values to be evaluated simultaneously.

The example above can be coded much more simply using the

PDFIntegrator.stats() method to evaluate the

expectation value of function f(p) (rather

than f_f2(p) above):

# want expectation value of f(p)

def f(p):

a = p['a']

b = p['b']

fp = a[0] * a[1] + 3 * b

return dict(a=a, b=b, fp=fp)

r = g_ev.stats(f)

print('results =', r)

print (' f(g) =', f(g))

print('\ncorrelation matrix:')

print(gv.evalcorr([r['a'][0], r['a'][1], r['b'], r['fp']]))

stats(f) calculates both the mean values and the standard deviations of

each component of f(p), combining them into gvar.GVar objects.

(The standard deviations include the uncertainties coming from the integration

added in quadrature with the uncertainties coming from the distribution.)

The output from this code compares the actual means and standard deviations

from g_ev.stats(f) with what is obtained from the Gaussian

approximation (f(g)):

results = {'a': array([2.0(1.0), 1.0(1.0)], dtype=object), 'b': 1.00(58), 'fp': 6.0(3.7)}

f(g) = {'a': array([2.0(1.0), 1.0(1.0)], dtype=object), 'b': 1.00(80), 'fp': 5.0(3.8)}

correlation matrix:

[[ 1.00000000e+00 9.90034523e-01 -3.17798188e-04 7.96573054e-01]

[ 9.90034523e-01 1.00000000e+00 -6.21970730e-04 7.99212165e-01]

[-3.17798188e-04 -6.21970730e-04 1.00000000e+00 4.63514253e-01]

[ 7.96573054e-01 7.99212165e-01 4.63514253e-01 1.00000000e+00]]

This shows that the results for f['a'] agree with the inputs (as expected because

they are Gaussian), but this is less true for r['b'] and r['fp'] whose

distributions are less well approximated by a Gaussian.

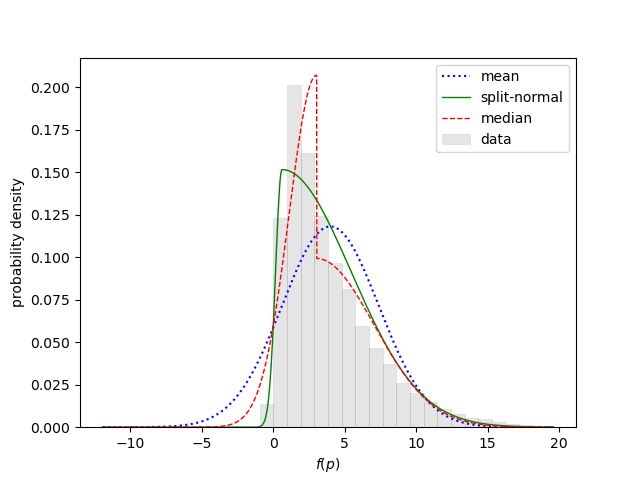

Additional information can be obtained by setting the keyword arguments moments

and/or histograms equal to True in PDFIntegrator.stats(). The code

r = g_ev.stats(f, moments=True, histograms=True)

print('Statistics for fp:')

print(r.stats['fp'])

plt = r.stats['fp'].plot_histogram().show()

plt.xlabel('a[0] * a[1] + 3 * b')

plt.show()

shows the statistical analysis for fp:

Statistics for fp:

mean = 5.9941(57) sdev = 3.732(12) skew = 1.166(18) ex_kurt = 2.264(99)

split-normal: 3.4084(64) +/- 4.765(11)/1.7320(57)

median: 5.3598(57) +/- 4.048(15)/2.8818(88)

g_ev.stats(f, moments=True, histograms=True) calculates

moments for each output quantity, and uses the moments to determines

the mean, standard deviation, skewness, and excess kurtosis of each distribution. It also

calculates a histogram for each distribution and fits the histogram with two

two-sided Gaussian models: one that is continuous (split-normal), and the other

that is discontinuous centered on the median. The uncertainties shown for

each quantity come from the vegas integrations.

The last line in

the code above displays the histogram

for fp, which confirms that it is not quite Gaussian:

The discussion in Case Study: Bayesian Curve Fitting illustrates how

vegas.PDFIntegrator can be used with a non-Gaussian PDF in two

examples, one with 4 parameters

and the other with 22 parameters. It also shows how to

use vegas.PDFIntegrator.sample() to create (weighted)

random samples of parameter points whose density is proportional

to the integrator’s PDF.

Finally, note that the lsqfit

Python module uses vegas.PDFIntegrator to implement a least-squares

fitter vegas_fit

that uses Bayesian integration (rather than minimization).

Faster Integrands¶

The computational cost of a realistic multidimensional integral

comes mostly from

the cost of evaluating the integrand at the Monte Carlo sample

points. Integrands written in pure Python are probably fast

enough for problems where neval=1e3 or neval=1e4 gives

enough precision. Some problems, however, require

hundreds of thousands or millions of function evaluations, or more.

We can significantly reduce the cost of evaluating the integrand

by using vegas’s batch mode and numpy vectors. For example,

the following code runs in about 58 min (on a 2024 laptop):

import vegas

import numpy as np

def ridge(x):

" Ridge of N Gaussians distributed along part of the diagonal. "

dim = len(x)

N = 1000

norm = (100. / np.pi) ** (dim / 2.) / N

ans = 0

for x0 in np.linspace(0.25, 0.75, N):

dx2 = (x[0] - x0) ** 2

for d in range(1, dim):

dx2 += (x[d] - x0) ** 2

ans += np.exp(-100. * dx2)

return ans * norm

integ = vegas.Integrator(4 * [[0, 1]])

warmup = integ(ridge, nitn=10, neval=2e5)

result = integ(ridge, nitn=10, neval=2e5, adapt=False)

print('result = %s Q = %.2f' % (result, result.Q))

It generates the following output:

result = 0.99987(29) Q = 0.81

Adding a decorator to the integrand function ridge(x)

@vegas.rbatchintegrand

def ridge(x):

...

reduces the run time to 20 sec, which is more than 170 times faster.

The decorator instructs vegas to present integration points to

the integrand in batches of approximately 50,000 points

(vegas parameter min_neval_batch)

rather than offering them one at a time.

Here, for example, function ridge(x) with the decorator

takes as its argument an array of integration

points — x[d, i] where d=0... labels the direction and

i=0... the integration point — and returns an array of integrand

values ans[i] * norm corresponding to those points. As a result

the code uses numpy vectorization to evaluate the integrand

for all 50,000 integration points in the batch at the same time, which is

much faster than handling the points separately.

The loop in the integrand could have been rewritten

for x0 in np.linspace(0.25, 0.75, N):

dx2 = (x[0, :] - x0) ** 2

for d in range(1, dim):

dx2[:] += (x[d, :] - x0) ** 2

ans[:] += np.exp(-100. * dx2[:])

to make the batch index explicit (:); here x[d],

dx2, and ans are all numpy arrays with

50,000 values, one for each integration point. Typically

one must modify the integrand

code to deal with the extra index i

when adding a batch decorator, but that wasn’t

necessary in ridge because trailing indices can be

left implicit in numpy arrays.

The advantage gained from using vegas’s batch mode

(with numpy vectorization)

is particularly

large in this example because the integrand is quite expensive to evaluate.

The original (non-batch) integral runs 160 times faster when N is

decreased from N=1000 to N=1. Batch mode is

still faster then, but by a more modest factor of about 50.

An alternative to a function decorated with vegas.rbatchintegrand() is

a class, derived from vegas.RBatchIntegrand, that behaves

like a batch integrand:

import vegas

import numpy as np

class batch_ridge(vegas.RBatchIntegrand):

def __init__(self, dim):

self.dim = dim

self.N = 1000

self.norm = (100. / np.pi) ** (self.dim / 2.) / self.N

self.x0array = np.linspace(0.25, 0.75, self.N)

def __call__(self, x):

" Ridge of N Gaussians distributed along part of the diagonal. "

ans = 0

for x0 in self.x0array:

dx2 = (x[0] - x0) ** 2

for d in range(1, self.dim):

dx2 += (x[d] - x0) ** 2

ans += np.exp(-100. * dx2)

return ans * self.norm

ridge = batch_ridge(dim=4)

integ = vegas.Integrator(ridge.dim * [[0, 1]])

warmup = integ(ridge, nitn=10, neval=2e5)

result = integ(ridge, nitn=10, neval=2e5, adapt=False)

print('result = %s Q = %.2f' % (result, result.Q))

This version is as fast as the previous batch integrand, but is potentially more flexible because it is built around a class rather than a function.

Batch mode is also useful for array-valued and dictionary-valued integrands. For example, the following two integrands (see Multiple Integrands Simultaneously) are equivalent:

def f(x):

dx2 = 0.0

for d in range(4):

dx2 += (x[d] - 0.5) ** 2

f = np.exp(-200 * dx2)

return [f, f * x[0], f * x[0] ** 2]

@vegas.rbatchintegrand

def f_rbatch(x):

dx2 = 0.0

for d in range(4):

dx2 += (x[d] - 0.5) ** 2

f = np.exp(-200 * dx2)

return [f, f * x[0], f * x[0] ** 2]

But the second integrand is much faster because again dx2, x[d],

and f

are all numpy arrays — dx2[:], x[d, :], and f[:] —

so that the entire batch of integration points is processed at the same

time. The array returned by f_rbatch(x) has an additional index

(on the right) labeling the integration point.

The batch integrands above have the batch index in the last/rightmost

position.

It is sometimes more convenient to have the batch index

be the first/leftmost index

rather than the last. Then @vegas.rbatchintegrand should be

replaced by @vegas.lbatchintegrand, and vegas.RBatchIntegrand by

vegas.LBatchIntegrand. The lbatch version of the integrand f(x)

above is:

@vegas.lbatchintegrand

def f_lbatch(x):

dx2 = 0.0

for d in range(4):

dx2 += (x[:, d] - 0.5) ** 2

f = np.exp(-200 * dx2)

ans = np.empty((x.shape[0], 3), float)

for n in range(3):

ans[:, n] = f * x[:, 0] ** n

return ans

Note where the batch index must be explicit here (x[:,d] and ans[:, n]),

unlike in the rbatch version.

The batch integrands above are fast because they are expressed in terms of

numpy operators that act on entire arrays.

That optimization is not always possible or simple. It is unnecessary if

we use the numba Python module to compile the integrand. Returning

to the ridge integral above, for example, a numba implementation

would be:

import numpy as np

import vegas

import numba

@vegas.lbatchintegrand

@numba.njit

def ridge(xbatch):

" Ridge of N Gaussians distributed along part of the diagonal. "

dim = xbatch.shape[1]

N = 1000

norm = (100. / np.pi) ** (dim / 2.) / N

ans = np.zeros(len(xbatch), dtype=float)

for i in range(len(xbatch)):

# iterate over each integration point x in xbatch

x = xbatch[i]

for j in range(N):

x0 = 0.25 + 0.5 * j / (N - 1)

dx2 = (x[0] - x0) ** 2

for d in range(1, dim):

dx2 += (x[d] - x0) ** 2

ans[i] += np.exp(-100. * dx2)

ans[i] *= norm

return ans

integ = vegas.Integrator(4 * [[0, 1]])

warmup = integ(ridge, nitn=10, neval=2e5)

result = integ(ridge, nitn=10, neval=2e5, adapt=False)

print('result = %s Q = %.2f' % (result, result.Q))

Here the decorator @numba.njit causes the ridge function to be

compiled into efficient machine code the first time it is called, and

the machine code is used in place of the Python function for that

and all subsequent calls. numba is particularly effective when

compiling low-level code such as this, where standard numerical

datatypes (integers, floats) are manipulated directly (rather than

relying on numpy array operations). This code is somewhat

faster than the batch integrands above that use numpy array

arithmetic (15 sec versus 20 sec).

There are a variety of other ways to create optimized codes using compilers. Some of these are discussed below in the section on Compiled Integrands for Speed; GPUs.

Multiple Processors¶

vegas supports parallel evaluation of integrands

on multiple processors. This

can shorten execution time substantially when the integrand is

costly to evaluate. Returning to the ridge example from the

previous section, the following code

runs almost six times faster

when using nproc=8 processors instead of the

default nproc=1 (on a 2024 laptop):

import numpy as np

import vegas

@vegas.rbatchintegrand

def ridge(x):

" Ridge of N Gaussians distributed along part of the diagonal. "

dim = len(x)

N = 1000

norm = (100. / np.pi) ** (dim / 2.) / N

ans = 0

for x0 in np.linspace(0.25, 0.75, N):

dx2 = (x[0] - x0) ** 2

for d in range(1, dim):

dx2 += (x[d] - x0) ** 2

ans += np.exp(-100. * dx2)

return ans * norm

def main():

integ = vegas.Integrator(4 * [[0, 1]], nproc=8) # 8 processors

warmup = integ(ridge, nitn=10, neval=2e5)

result = integ(ridge, nitn=10, adapt=False, neval=2e5)

print('result = %s Q = %.2f' % (result, result.Q))

if __name__ == '__main__':

main()

One might have expected the code to run eight times faster

(instead of six), but it takes time to

initiate the nproc processes, and to feed data and

collect results from them.

Parallel processing only becomes useful when integrands are

sufficiently costly that such overheads become negligible.

Parallel processing is managed by Python’s

multiprocessing module.

The if __name__ == '__main__' construct at the end of

this code is essential when running on Windows or MacOS (in its

default mode) as it prevents additional processes being launched

when the main module is imported as part of spawning the nproc

processes; see the multiprocessing documentation for more

details. This is not an issue for Linux/Unix. It is also important

that the integrand and its return values can be pickled using

Python’s pickle module. This is the case for most pure

Python integrands.

The code above will generate an AttributeError when run in some

interactive environments (as opposed to running from the command line)

on some platforms. This can usually be fixed by putting the integrand

function ridge(x) into a file and importing it into the script.

vegas also supports multi-processor evaluation of integrands using MPI

(via the Python module mpi4py which must be installed separately).

Placing the code above in a file ridge.py, with mpi=True set

in the integrator (and with nproc=1 or unset) —

integ = vegas.Integrator(4 * [[0, 1]], mpi=True)

— ridge.py can be run on 8 processors using

mpirun -np 8 python ridge.py

The speedup is similar to that from using the

multiprocessing module, above.

Note that the random number generator used by vegas must be

synchronized so that it

produces the same random numbers on the different processors. This

happens automatically for the default random-number generator.

vegas’s batch mode makes it possible to implement other strategies

for distributing integrand evaluations across multiple processors.

For example, numba provides support for

parallel evaluation of specific loops. The numba version

of the ridge integrand (see previous section) can be

rewritten

import vegas

import numba

import numpy as np

@vegas.lbatchintegrand

@numba.njit(parallel=True)

def ridge(xbatch):

" Ridge of N Gaussians distributed along part of the diagonal. "

dim = xbatch.shape[1]

N = 1000

norm = (100. / np.pi) ** (dim / 2.) / N

ans = np.zeros(len(xbatch), dtype=float)

for i in numba.prange(len(xbatch)):

# iterate over each integration point x in xbatch

x = xbatch[i]

for j in range(N):

x0 = 0.25 + 0.5 * j / (N - 1)

dx2 = (x[0] - x0) ** 2

for d in range(1, dim):

dx2 += (x[d] - x0) ** 2

ans[i] += np.exp(-100. * dx2)

ans[i] *= norm

return ans

integ = vegas.Integrator(4 * [[0, 1]]) # leave nproc unset

# parallelization handled by ridge(x)

warmup = integ(ridge, nitn=10, neval=2e5)

result = integ(ridge, nitn=10, neval=2e5, adapt=False)

print('result = %s Q = %.2f' % (result, result.Q))

where function numba.prange is used instead of Python’s range function to

indicate that different iterations of the loop can be run in parallel

on multiple processors. numba uses

all processors available. The speedup for this example is similar to that using

the other multi-processor methods above.

As another example exploiting vegas’s batch mode,

we can create a class parallelintegrand

whose function is similar to decorator vegas.lbatchintegrand(),

but where Python’s

multiprocessing module provides parallel processing:

import multiprocessing

import numpy as np

import vegas

class parallelintegrand(vegas.LBatchIntegrand):

""" Convert (batch) integrand into multiprocessor integrand.

Integrand should return a numpy array.

"""

def __init__(self, fcn, nproc=4):

" Save integrand; create pool of nproc processes. "

super().__init__()

self.fcn = fcn

self.nproc = nproc

self.pool = multiprocessing.Pool(processes=nproc)

def __del__(self):

" Standard cleanup. "

self.pool.close()

self.pool.join()

def __call__(self, x):

" Divide x into self.nproc chunks, feeding one to each process. "

nx = x.shape[0] // self.nproc + 1

# launch evaluation of self.fcn for each chunk, in parallel

results = self.pool.map(

self.fcn,

[x[i*nx : (i+1)*nx] for i in range(self.nproc)],

1,

)

# convert list of results into a single numpy array

return np.concatenate(results)

Then fparallel = parallelintegrand(f, 4), for example, will create a

new integrand fparallel(x) that uses 4 CPU cores.

Sums with vegas¶

The ridge code in the previous sections is inefficient in the way it

handles the sum over N = 1000 Gaussians. It is not necessary to include every

term in the sum for every integration point. Rather we can sample the sum,

using vegas to do the sampling. The trick is to replace the sum with

an equivalent integral:

where  is the largest

integer smaller than . The

resulting integral can then be handed to

is the largest

integer smaller than . The

resulting integral can then be handed to vegas.

Using this trick,

the batch version of ridge integral from Faster Integrands can

be re-cast as a 5-dimensional

integral, where the integral over x[-1] does the sum over Gaussians:

import vegas

import numpy as np

@vegas.rbatchintegrand

def ridge(x):

""" Ridge of N Gaussians distributed along part of the diagonal.

Gaussians are at points x0[d] = 0.25 + 0.5 * i /(N-1) for

all directions d and Gaussians i=0...N-1.

"""

dim = len(x) - 1

N = 1000

norm = (100. / np.pi) ** (dim / 2.)

x0 = 0.25 + 0.5 * np.floor(x[-1] * N) / (N - 1)

dx2 = (x[0] - x0) ** 2

for d in range(1, dim):

dx2 += (x[d] - x0) ** 2

return np.exp(-100. * dx2) * norm

integ = vegas.Integrator(5 * [[0, 1]])

warmup = integ(ridge, nitn=10, neval=8e5)

result = integ(ridge, nitn=10, neval=8e5, adapt=False)

print('result = %s Q = %.2f' % (result, result.Q))

This code gives a result with the same precision as the earlier (batch) integral, but is 20 times faster (1 sec versus 20 sec).

The same trick can be generalized to sums over multiple indices, including sums

to infinity. vegas will provide Monte Carlo estimates of the sums, emphasizing

the more important terms.

Saving Results Automatically¶

Results returned by a vegas integrator can be pickled for later use using pickle.dump/load (or

gvar.dump/load) in the usual way. Results can also be saved automatically using the

save keyword to specify a file name for the pickled result: for example, running

import vegas

import math

def f(x):

dx2 = 0

for d in range(4):

dx2 += (x[d] - 0.5) ** 2

return math.exp(-dx2 * 100.) * 1013.2118364296088

integ = vegas.Integrator([[-2, 2], [0, 2], [0, 2], [0, 2]])

result = integ(f, nitn=10, neval=1000, save='save.pkl')

print(result.summary())

print('result = %s Q = %.2f' % (result, result.Q))

prints out

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 0.00050(45) 0.00050(45) 0.00 1.00

2 0.115(59) 0.00051(45) 3.77 0.05

3 0.66(22) 0.00051(45) 6.41 0.00

4 0.72(15) 0.00052(45) 12.27 0.00

5 0.97(12) 0.00053(45) 26.17 0.00

6 1.045(61) 0.00059(45) 79.46 0.00

7 1.016(45) 0.00069(45) 152.45 0.00

8 1.023(29) 0.00093(45) 307.32 0.00

9 0.999(20) 0.00141(45) 573.82 0.00

10 1.025(17) 0.00208(45) 896.20 0.00

result = 0.00208(45) Q = 0.00

but also stores result in file save.pkl. The result can be retrieved

later using, for example,

import pickle

with open('save.pkl', 'rb') as ifile:

result = pickle.load(ifile)

print(result.summary())

print('result = %s Q = %.2f' % (result, result.Q))

which gives exactly the same output.

This feature is most useful for expensive integrations, ones taking minutes or hours

to complete. This is because the pickled file is updated after every vegas

iteration. This means that a short script like the one above can be used to

monitor progress before the integration is finished. It also means that results

up through the most recent iteration are saved even if the integration is

terminated early or crashes.

Saved results are also useful because they can be fixed after the code has

finished running.

The early iterations in the output above are clearly wrong

and badly distort the weighted average. The problem is that vegas isn’t well

adapted to the integrand until around the fifth or sixth iteration. We

can discard the first five iterations (from the saved result)

by using function vegas.ravg()

to redo the weighted average:

import pickle

import vegas

with open('save.pkl', 'rb') as ifile:

result = pickle.load(ifile)

result = vegas.ravg(result.itn_results[5:])

print(result.summary())

print('result = %s Q = %.2f' % (result, result.Q))

This gives the following output

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 1.045(61) 1.045(61) 0.00 1.00

2 1.016(45) 1.026(36) 0.14 0.71

3 1.023(29) 1.024(23) 0.07 0.93

4 0.999(20) 1.010(15) 0.28 0.84

5 1.025(17) 1.017(11) 0.31 0.87

result = 1.017(11) Q = 0.87

which is greatly improved over the original.

It is also possible to save an adapted integrator using pickle.dump/load

(or gvar.dump/load). This can also be done automatically, by

replacing, for example, save='save.pkl' with saveall='saveall.pkl'

in the script above. The pickled file then returns a tuple containing

the most recent result and integ. Having the (adapted) integrator,

it is possible to further refine a result later: for example, running

import pickle

def f(x):

dx2 = 0

for d in range(4):

dx2 += (x[d] - 0.5) ** 2

return math.exp(-dx2 * 100.) * 1013.2118364296088

with open('saveall.pkl', 'rb') as ifile:

result, integ = pickle.load(ifile)

result = vegas.ravg(result.itn_results[5:])

new_result = integ(f, nitn=5)

print('\nNew results:')

print(new_result.summary())

print('\nCombined results:')

result.extend(new_result)

print(result.summary())

print('Combined result = %s Q = %.2f' % (result, result.Q))

significantly improves the final result by adding 5 additional

iterations

to what was done earlier. The new iterations are in new_result

and tabulated under “New Results” in the output:

New results:

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 1.007(17) 1.007(17) 0.00 1.00

2 1.006(14) 1.007(11) 0.00 0.98

3 0.997(13) 1.0029(82) 0.16 0.85

4 1.015(21) 1.0044(76) 0.20 0.90

5 0.990(13) 1.0007(66) 0.39 0.82

Combined results:

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 1.045(61) 1.045(61) 0.00 1.00

2 1.016(45) 1.026(36) 0.14 0.71

3 1.023(29) 1.024(23) 0.07 0.93

4 0.999(20) 1.010(15) 0.28 0.84

5 1.025(17) 1.017(11) 0.31 0.87

6 1.007(17) 1.0136(94) 0.30 0.91

7 1.006(14) 1.0114(78) 0.28 0.95

8 0.997(13) 1.0076(66) 0.36 0.92

9 1.015(21) 1.0082(63) 0.33 0.95

10 0.990(13) 1.0047(57) 0.48 0.89

Combined result = 1.0047(57) Q = 0.89

The new results are merged onto the end of the original results using

result.extend(new_result) to obtain the combined results from all

10 iterations (old plus new).

Saving integrators is again useful for costly

integrations that might need to be restarted later since the saved integrator

remembers the variable transformations made to minimize errors, and

so need not be readapted to the integrand when used again. The resulting

pickle file can be large, however, particularly if neval is large.

The (adapted) vegas.AdaptiveMap integ.map can also

be pickled by itself and results in a smaller file.

vegas Maps and Preconditioning vegas¶

vegas adapts by remapping the integration variables (see Importance Sampling). It

is possible to precondition this map, before creating a vegas.Integrator.

Preconditioned maps can improve vegas results when

much is known about the integrand ahead of time. Consider,

for example, the integral

which has high, narrow peaks at

Given the locations of the peaks we can create a vegas map before integrating

that emphasizes the regions around them:

import vegas

import numpy as np

@vegas.batchintegrand

def f(x):

ans = 0

for c in [0.45, 0.7]:

dx2 = np.sum((x - c) ** 2, axis=1)

ans += np.exp(-50 * np.sqrt(dx2))

return ans * 247366.171

dim = 5

map = vegas.AdaptiveMap(dim * [[0, 1]]) # uniform map

x = np.concatenate([ # 2000 points near peaks

np.random.normal(loc=0.45, scale=3/50, size=(1000, dim)),

np.random.normal(loc=0.7, scale=3/50, size=(1000, dim)),

])

map.adapt_to_samples(x, f(x), nitn=5) # precondition map

integ = vegas.Integrator(map, alpha=0.)

r = integ(f, neval=1e4, nitn=5)

print(r.summary())

vegas maps are objects of type vegas.AdaptiveMap. Here we

create a uniform map object map. We then

generate 2000 random points x from normal distributions centered around

the peak locations. map.adapt_to_samples(x, f(x), nitn=5) optimizes

the map for integrating f(x) based on information about the integrand

at the random

points x. As a result, vegas is almost fully adapted to the

integrand already in its first iteration:

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 0.981(25) 0.981(25) 0.00 1.00

2 0.983(11) 0.9825(98) 0.00 0.96

3 1.001(10) 0.9915(71) 0.85 0.43

4 1.000(13) 0.9933(63) 0.67 0.57

5 0.993(11) 0.9931(54) 0.50 0.74

We set alpha=0 in the integrator to prevent

further changes to the pre-adapted map.

These results can be contrasted with what happens without preconditioning, where the integrator is still far from converged by the fifth iteration:

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 0.74(27) 0.74(27) 0.00 1.00

2 0.93(12) 0.90(11) 0.38 0.54

3 0.94(10) 0.920(74) 0.23 0.79

4 1.091(75) 1.004(53) 1.03 0.38

5 1.063(58) 1.031(39) 0.91 0.46

The exact distribution of random points x isn’t important; what

matters is that they cover and are concentrated in

the dominant regions contributing to the integral. Should it be needed,

a sample xsample=(x, f(x))

in x-space is easily converted to the equivalent sample in y-space using:

x, fx = xsample

y = np.empty(x.shape, float)

jac = np.empty(x.shape[0], float)

map.invmap(x, y, jac)

ysample = (y, jac * fx)

where map.invmap(x, y, jac) fills array y with the y-space

points corresponding to x, and array jac with the transformation’s

Jacobian.

Note that vegas maps can be used with integrators other than vegas.

The vegas map maps the integration variables x[d] into

new variables y[d] (where 0 < y[d] < 1) that make the integrand

easier to integrate. The integrator is used

to evaluate the integral in y-space. To illustrate how this

works, we replace the last three lines of the code at the start of

this section with

the following:

def smc(f, neval, dim):

" integrates f(y) over dim-dimensional unit hypercube "

y = np.random.uniform(0,1, (neval, dim))

fy = f(y)

return (np.average(fy), np.std(fy) / neval ** 0.5)

def g(y):

jac = np.empty(y.shape[0], float)

x = np.empty(y.shape, float)

map.map(y, x, jac)

return jac * f(x)

# with map

r = smc(g, 50_000, dim)

print(' SMC + map:', f'{r[0]:.3f} +- {r[1]:.3f}')

# without map

r = smc(f, 50_000, dim)

print('SMC (no map):', f'{r[0]:.3f} +- {r[1]:.3f}')

Here smc is a Simple Monte Carlo (SMC) integrator and g(y) is the

integrand in y-space that corresponds to f(x) in x-space.

The mapping is done by map.map(y, x, jac) which fills the arrays

x and jac with the x values and Jacobian corresponding

to integration points y. The result is

SMC + map: 1.013 +- 0.020

SMC (no map): 1.703 +- 0.535

where we give results from SMC with and without using

the vegas map. The vegas map greatly improves

the SMC result, which, not surprisingly, is significantly

less accurate the the vegas result above.

Maps for use with other integrators can be built

directly, as above, or they can be built for a particular

integrand by running several iterations of vegas with

the integrand and using the vegas integrator’s map: integ.map.

vegas Stratifications¶

Having mapped the integration variables x[d] to new variables y[d],

vegas evaluates the integral in y-space using stratified Monte

Carlo sampling (see Adaptive Stratified Sampling). This is

done by dividing each axis d into nstrat[d] equal strata,

which divide the D-dimensional integration volume into

prod(nstrat) sub-volumes or (rectangular) hypercubes. vegas does a

separate integral

in each hypercube, adjusting the number of integrand evaluations

used in each one to minimize errors. By default, the number of

strata in each direction is set automatically based on the number

neval of integrand evaluations per iteration: nstrat[d] is set

equal to  for the first

for the first  directions

and

directions

and  for

the remaining directions, where

and are chosen

to maximize the number strata consistent with

for

the remaining directions, where

and are chosen

to maximize the number strata consistent with neval.

It is also possible, however, to specify the number of

strata nstrat[d] for each direction separately.

Requiring (approximately) the same number of strata in each direction

greatly limits the number of strata per direction in very high

dimensions, since the product of the nstrat[d] must be

less than neval/2 (so there are at least two integrand

samples in each hypercube). This restricts vegas’s ability to

adapt. Often there is a subset of integration directions

that are more challenging than the others. In high

dimensions (and possibly lower dimensions)

it is worthwhile using larger values

for nstrat[d] for those directions.

An example is the 20-dimensional integral

which has high, narrow peaks at

These peaks are aligned along the diagonal of the integration volume for the first five directions, but are on top of each other in the remaining directions. This makes the integrals over the first five directions much more challenging than the remaining integrals.

The following code compares an integral that uses the default stratification

from vegas with one that concentrates all of the strata in the first

five directions:

import vegas

import numpy as np

dim = 20

rlist = np.array([

5 * [0.23] + (dim - 5) * [0.45],

5 * [0.39] + (dim - 5) * [0.45],

5 * [0.74] + (dim - 5) * [0.45],

])

@vegas.batchintegrand

def f(x):

ans = 0

for r in rlist:

dx2 = np.sum((x - r[None, :]) ** 2, axis=1)

ans += np.exp(-100 * dx2)

return ans * 356047712484621.56

nitn = 5

neval = 2e6

integ = vegas.Integrator(dim * [[0, 1]])

integ(f, neval=neval, nitn=20) # training

# default stratification

result1 = integ(f, nitn=nitn)

print(f'DEFAUlT: nstrat = {np.array(integ.nstrat)} ({np.prod(integ.nstrat)})')

print(result1.summary())

# stratification concentrated in first 5 directions

nstrat = 5 * [10] + (dim - 5) * [1]

result2 = integ(f, neval=neval, nstrat=nstrat)

print(f'MODFIED: nstrat = {np.array(integ.nstrat)} ({np.prod(integ.nstrat)})')

print(result2.summary())

This code generates the following output:

DEFAULT: nstrat = [2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 1 1 1] (131072)

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 0.999(11) 0.999(11) 0.00 1.00

2 1.023(11) 1.0107(79) 2.40 0.12

3 0.9922(93) 1.0029(60) 2.37 0.09

4 1.0054(92) 1.0037(50) 1.60 0.19

5 1.0054(88) 1.0041(44) 1.20 0.31

MODIFIED: nstrat = [10 10 10 10 10 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1] (100000)

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 1.0045(26) 1.0045(26) 0.00 1.00

2 0.99968(87) 1.00016(83) 3.02 0.08

3 0.9994(10) 0.99986(65) 1.68 0.19

4 0.99940(67) 0.99964(47) 1.20 0.31

5 0.99957(56) 0.99961(36) 0.90 0.46

The default stratification has 2 strata in almost every direction, while the modified stratification has 10 strata in each of the first 5 directions, but only 1 in all other directions. The latter is 10–15 times more accurate.

In more realistic examples, we may not know which are the most challenging directions;

then function vegas.restratify() might be useful. This function tries

to determine which directions are more challenging than others, and uses this

information to create an new integrator with a stratification that emphasizes

the more difficult directions. Replacing the

last block of code in the example above with

# automatic re-stratification

integ = vegas.restratify(integ, f)

result2 = integ(f)

print(f'MODIFIED: nstrat = {np.array(integ.nstrat)} ({np.prod(integ.nstrat)})')

print(result2.summary())

gives in the following result:

MODIFIED: nstrat = [12 9 13 9 10 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1] (126360)

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 0.99823(93) 0.99823(93) 0.00 1.00

2 1.00007(85) 0.99923(63) 2.14 0.14

3 0.99903(62) 0.99913(44) 1.10 0.33

4 0.99939(61) 0.99922(36) 0.77 0.51

5 0.99876(61) 0.99910(31) 0.68 0.60

The modified code replaces integrator integ by a new integrator with an improved stratification, which turns out to be quite similar to the improved stratification we used above. Again results are more than ten times as accurate as with the default stratification.

vegas Jacobian¶

The vegas Jacobian is useful when integrating multiple integrands simultaneously

when some of the integrands depend only on a subset of the integration variables.

Consider, for example, the integral

We want to compare this integral for two different cases: a)

where  is a random number near zero drawn from a distribution

proportional to

is a random number near zero drawn from a distribution

proportional to  with

with  ;

and b) where

;

and b) where  . The result for the first case is

. The result for the first case is

where

where

The result for the second case is

The first two integrals should have very similar dependence on  , while

the first and third integrals should have similar dependence on

, while

the first and third integrals should have similar dependence on  .

Given these similarities, we would like to do all three integrals simultaneously;

but one integral is two-dimensional and the other two are one-dimensional.

.

Given these similarities, we would like to do all three integrals simultaneously;

but one integral is two-dimensional and the other two are one-dimensional.

One solution is to turn the one-dimensional integrals into two-dimensional

integrals by rewriting  as

as

and similarly for  .

These are then easily integrated together —

.

These are then easily integrated together —

import vegas

import numpy as np

integ = vegas.Integrator(2 * [(0., np.pi/2.)])

@vegas.rbatchintegrand

def f(x):

Ia_num = np.exp(-1e2 * np.sin(x[1])) / ((x[0] - x[1])**2 + 0.01)

Ia_den = np.exp(-1e2 * np.sin(x[1])) / (np.pi/2)

Ib = 1 / (x[0]**2 + 0.01) / (np.pi/2)

return dict(Ia_num=Ia_num, Ia_den=Ia_den, Ib=Ib)

w = integ(f, neval=20000, nitn=10)

r = integ(f, neval=20000, nitn=5)

print(r.summary(True))

print('Ia =', r['Ia_num'] / r['Ia_den'], 'Ia - Ib =', r['Ia_num'] / r['Ia_den'] - r['Ib'])

— but the result is useless:

itn integral wgt average chi2/dof Q

-------------------------------------------------------

1 0.160568(44) 0.160568(44) 0.00 1.00

2 0.160551(40) 0.160559(30) 0.13 0.94

3 0.160533(35) 0.160549(23) 0.36 0.90

4 0.160568(32) 0.160555(18) 0.96 0.47

5 0.160553(29) 0.160554(15) 0.73 0.72

key/index value

-----------------------------

Ia_num 0.160554 (15)

Ia_den 0.0099995 (60)

Ib 14.62 (88)

Ia = 16.0562(99) Ia - Ib = 1.43(88)

is almost 100x less accurate than  , despite

having an integrand with no

, despite

having an integrand with no x[1] dependence. The problem is that the

vegas map for x[1] is tailored to  , which has

a strong peak at

, which has

a strong peak at x[1]=0. That map is highly sub-optimal for integrating

a function, like that in , that is independent of x[1].

A much better approach is to rewrite the one-dimensional integrals

as two-dimensional integrals using the vegas

map’s Jacobian  in the extra direction

in the extra direction  .

For example,

.

For example,

This turns the integral into an integral over  with an integrand equal to 1. The Monte Carlo integral over

with an integrand equal to 1. The Monte Carlo integral over  in

in vegas is then exact; it is unaffected by the map for that direction.

This is easily implemented for both one-dimensional integrals by setting

keyword uses_jac=True in the integrator and modifying the integrand:

@vegas.rbatchintegrand

def f(x, jac):